The Deficit-Doubling Receipt: PBO Puts Carney’s Fiscal Brand on Trial

Carney promised financial seriousness. The budget watchdog just handed taxpayers a very different receipt.

Mark Carney’s central political sales pitch is competence: the former central banker who would bring discipline to Ottawa after years of Liberal overspending. The Parliamentary Budget Officer’s June outlook makes that brand much harder to sell.

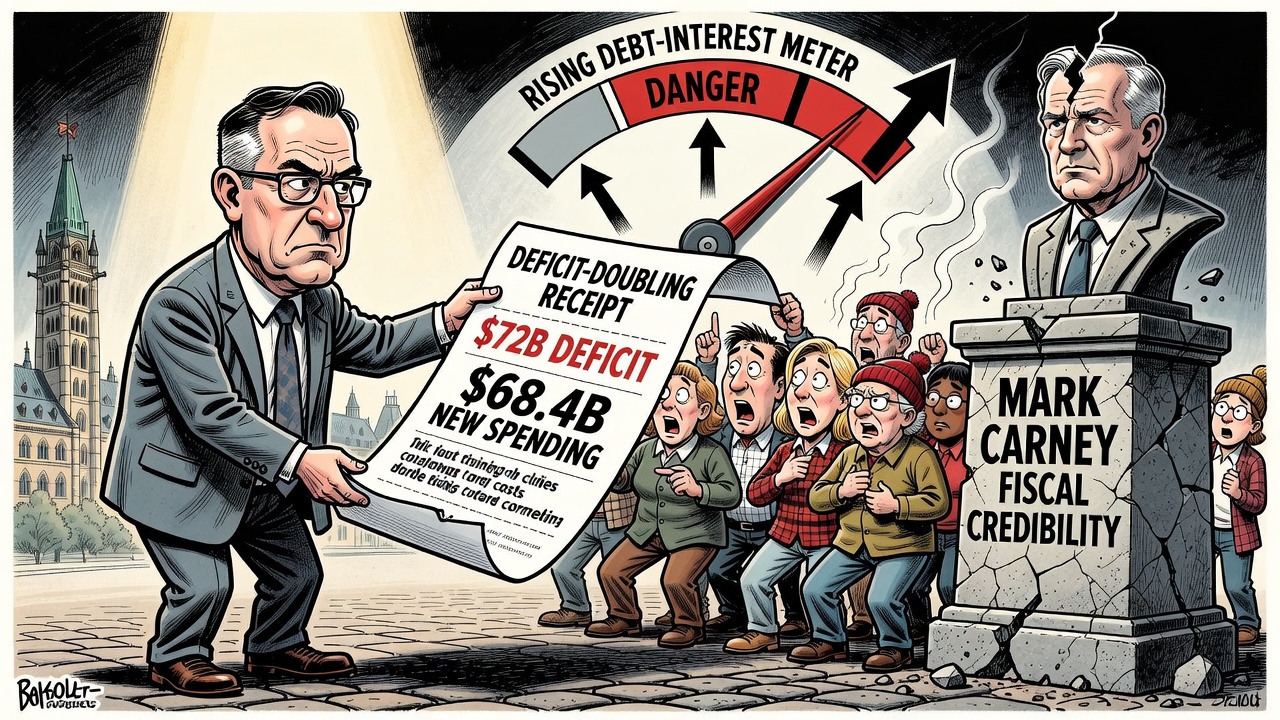

The PBO projects the federal deficit rising from $36.3 billion in 2024–25 to $72.0 billion in 2025–26. That is not a rounding error. It is a near doubling of the shortfall in a single fiscal year, with the watchdog pointing to expenses outpacing modest revenue growth and “largely reflecting” new measures.

The deeper problem is that this is not presented as a one-year emergency. PBO says deficits are projected to average around $64 billion over the next five years. Even if no new measures are introduced and temporary measures expire as scheduled, the deficit is still projected at $58.2 billion by 2030–31. That is not fiscal balance. That is permanent borrowing dressed up as management.

The source of the pressure is not mysterious. PBO’s status-quo outlook includes measures from Budget 2025 and the Spring Economic Update 2026, which together add $68.4 billion in net new spending from 2025–26 to 2030–31. Conservatives should say plainly what taxpayers already understand at the kitchen table: if you keep adding new bills while income growth slows, the credit card balance rises.

The growth assumptions make the picture worse. Treating the current U.S. tariff environment as permanent, PBO now projects real GDP growth of 1.1% in 2026 and 1.6% in 2027. Weaker growth means weaker revenues, and weaker revenues make every new promise more expensive. A government that calls itself prudent should be tightening priorities under those conditions, not widening the gap.

The Canadian Taxpayers Federation framed the issue as Carney going over budget twice: first above Budget 2025 in the spring update, then above the spring update in the PBO projection. Its tone is partisan, but the accountability question is fair: what is a budget worth if Ottawa treats it like a suggestion one month later?

Debt interest is the quiet tax on every future federal budget. PBO says the debt service ratio is projected to reach 13.1% by 2030–31. The Taxpayers Federation cites PBO numbers showing public debt charges per person rising to $1,885 by 2030. That money will not hire nurses, build homes, equip troops or lower taxes. It will service yesterday’s borrowing.

Carney did not create every fiscal problem he inherited. But he owns the choices made under his government, his budget and his update. If Ottawa wants Canadians to believe the banker is back in charge, it should start by producing a real restraint plan: program-by-program savings, hard spending caps, a path to balance, and monthly public reporting against the budget.

Until then, the receipt is clear: higher deficits, weaker growth, more spending, and taxpayers stuck with the interest bill.

- Parliamentary Budget Officer: Updated outlook projects weaker growth and higher deficits

- Parliamentary Budget Officer: Economic and Fiscal Outlook — June 2026

- Canadian Taxpayers Federation: Carney goes over budget — twice

This article uses official PBO projections as the primary factual basis and identifies the Canadian Taxpayers Federation as an advocacy/accountability source where its interpretation is discussed.